Dear Readers,

It's been over a month since I wrote a post -- what a crazy month! I've had several job interviews, so I've been crazy busy preparing for those, and I'm making great strides on the creative writing project I'm working on. That being said, what a crazy time in the markets this past month! Actually, I should state that more accurately: what a crazy time in the government this past month!

The U.S. government officially shut down on Tuesday, October 1 since Congress and the White House couldn't come to an impasse on funding Obamacare (which has already been made a law and been defended by the Supreme Court). This means that a lot of services are not available, national parks are closed, and, most unfortunately, some people are not getting the public assistance they rely on.

The shutdown is a big deal, but the market didn't really react to it, implying that investors don't really think it's a big deal. Consensus seems to be that it's about the egos of the leaders of the Republican party, primarily. I agree with that on one hand; however, the country is not run by Republicans alone, so Democrats are not innocent in this debacle. But, politically, the fallout appears to have wounded the reputation Republicans much more -- it's approval rating is at just 28%, the lowest in the history of Gallup polling (which, to be honest, isn't all that long; they've only been polling this for 21 years). This could certainly favor Democrats in the next round of elections, but that's over a year away. It could have the most positive impact on the Democratic presidential candidate. Favorable buzz is already beginning to swarm around Hilary Rodham Clinton for her possible run in 2016.

But back to the markets. As I said, the markets didn't even flinch at the shutdown. BUT it freaked out at the possibility of the U.S. hitting the debt ceiling and defaulting on its obligations. Default means that interest rates will rise rapidly because, suddenly, the U.S. has become riskier and investors demand to be compensated for risk.

The rest of the world is on edge about how the U.S. will resolve this issue because U.S. Treasury rates effect so many other rates around the world, and many holders of Treasuries live outside of the U.S. Actually, the Chinese government is the largest U.S. creditor, holding $1.3 trillion of Treasuries. As a result, officials in Beijing have stressed, like a mother of arguing siblings, that the U.S. had better figure itself out sooner rather than later.

Congress and the White House have only 3 days, until October 17, to come to a consensus. Needless to say, political agendas should not put the world markets in jeopardy. Now, the world waits to see who will be the bigger person in government.

Monday, October 14, 2013

Tuesday, September 3, 2013

Read My Lips: My favorite books on investing

As any Amazon.com lover knows, there are a ton of books out

there covering every subject known to man. Same goes for investing books. I

mean, I am amazed at the number of books on investing exist, not even counting

the ones that speak about personal finance more generally.

Despite the number of pickings, you definitely shouldn’t

cast them all aside – investing greats learned everything they know from the

best books written on the topic. So which ones are worthwhile?

The most famous, and arguably the best, book ever written on

investing is The Intelligent Investor by Benjamin Graham. Graham was Warren Buffett’s (arguably the greatest investor that ever lived) teacher at Columbia

University and investing guru. Graham strongly believed in buying stocks that are

undervalued, or selling for less than their assets are worth. The Intelligent

Investor breaks down this philosophy in excruciating detail. It’s actually the

layman’s version of Graham’s investing textbook, Security Analysis. That said,

I’ll admit that it is a bit dry; in fact, one of my best professors in college

gave me the book during my senior year (2006) and I’m only just now (2013)

getting past chapter 1. Yes, it is dense and academic, but if you’re super

serious about investing, it’s a must-read.

The next most famous, in my opinion, is A Random Walk Down Wall Street by Burton Malkiel, a gem that was first published in the 1970s. I’d

recommend this to ordinary investors because it covers an exhaustive range of

information, but is so well-written and easy to digest. I gobbled it up like a

novel. Malkiel purports that there is no point in trying to select individual

stocks in order to “beat” the market because, ultimately, the market is going

to outperform any manager. That being said, he advises investors to stick to

index-based mutual funds. I found his argument very convincing and changed the

way I thought about my (well, my husband’s, for right now) 401K allocation.

One that I encountered recently and found very helpful was

the Motley Fool’s Million Dollar Portfolio by David and Tom Gardner. The Motley Fool is an

excellent website, exploding with investing information, and is very well

respected in the industry. Tom and David, the brothers who founded the site, explain

portfolio building and management in clear, entertaining terms in MDP. It’s definitely

not as long as the Intelligent Investor or A Random Walk, so if you want the

juicy bits in a short amount of time, go for it! The tone is friendly and

approachable, but it doesn’t just stick to giving basic information. The best part is the corresponding website, which keeps the book current -- definitely a plus among books that recommend specific stocks in this crazy, volatile world. (Unfortunately, the website is not accepting new members, but will soon, hopefully.)

Last, for the risk-averse among us, I’d recommend Zvi Bodie’s

Worry-Free Investing. The book is smaller than it looks since the print is

humongous and it has lots of graphics to make complex points perfectly clear.

It lays out the simplest investment portfolio recommendations I’ve ever

encountered in a book, but still covers next-step-up topics like derivatives

and Treasury Inflation-Protected Securities. Great for investors who are really only interested in saving for retirement.

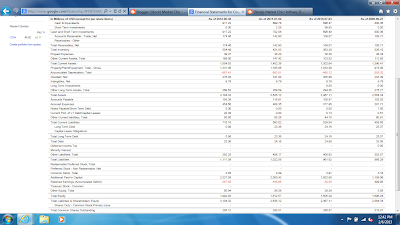

Since sometimes you’ll probably want to invest in a single

stock, it’s good to know how to read financial statements. While my blogposts

(here, here, and here) gave some information, you should become more familiar. For a brief, but

in-depth overview of accounting concepts, try Financial Intelligence by Karen Berman. It

says it’s for managers who do not work in financial services, but it is simple

enough for someone with no business experience to understand.

As you all know, we

recently weathered the worst financial crisis since the Great Depression. While

there’s plenty of theories out there about who to blame for it, there are some

clear sequences of events that led up to it. A great recounting and explanation

can be found in Roger Lowenstein’s The End of Wall Street. Lowenstein’s writing

style is unintimidating, but can be a little Wall Street-bashing, if you don’t

mind that. If you do, I think you’d love Michael Lewis’s Liar’s Poker, the

tell-all that reads like a novel and is supposed to be a cautionary tale, but

only excites undergrads around the world about joining the ranks of the Street.

Well, those are my picks. What are some investing reads you

all have found helpful or even entertaining?

Sunday, August 18, 2013

My Passion, My Life

I recently signed up to volunteer with an organization called Operation HOPE, which teaches kids and young adults across the country financial literacy. It's a great organization, and I can't wait to volunteer!

When the volunteers and I introduced ourselves on our conference call, we were asked to tell what made us interested in volunteering to teach financial literacy. Answers ranged from wanting to meet more people with similar interests to paying forward what was learned from mistakes. While I found myself in both camps, the second resonated with me so strongly, it made me physically tremble.

When I think about why I've so passionately pursued a job in financial services, I remember why I started this blog: I've made financial mistakes in my past, many of which I learned from my family's behavior, and now that I've learned from them, I want to be a positive role model to my friends, family, and the next generation.

I realized that the first step to financial independence isn't getting out of student loan debt. That's definitely one of the first steps, and HUGE, so I'm not counting it out, but there is something bigger that comes before it: dignity. I found it wonderful that Operation HOPE begins by teaching students about dignity, or "the quality or state of being worthy, honored, or esteemed."

If we have never experienced it -- or really seen it -- do we really feel worthy of financial independence?

That feeling of worth is what drives my desire to succeed, which fuels my desire to learn constantly more about investing, which will help me achieve financial independence.

Over the years, as I've learned more about investing, I've seen more of the ways it enhances wealth in all aspects of society, not just for people. Take your favorite museum, for example. Let's say the Museum of Modern Art. It has an endowment, or a massive investment account that helps them fund the operation.

The endowment is run by professional investors whose primary goal is sustaining the museum's wealth, so it can grow its collection and reach more people. Think about the kids who go to MoMA, whose minds are opened to the world's infinite possibilities, maybe even what they can be when they grow up. A trip to MoMA might a temporary moment of escape for a kid from a not-so-great life situation. To think, the endowment managers get to invest and change lives by supporting the arts for a living -- I can't think of a better career!

To me, investing provides not only a door to financial independence, but to a satisfying career. I want to continue creating and maintaining sustainable wealth for institutional and high net worth investors who are changing thousands of lives. Through this blog, I hope to make my own little mark in the lives of my friends and family. :)

--

In my next post, I'll resume the education: With the bazillions of investing books out there, which ones are actually worth reading?

When the volunteers and I introduced ourselves on our conference call, we were asked to tell what made us interested in volunteering to teach financial literacy. Answers ranged from wanting to meet more people with similar interests to paying forward what was learned from mistakes. While I found myself in both camps, the second resonated with me so strongly, it made me physically tremble.

When I think about why I've so passionately pursued a job in financial services, I remember why I started this blog: I've made financial mistakes in my past, many of which I learned from my family's behavior, and now that I've learned from them, I want to be a positive role model to my friends, family, and the next generation.

I realized that the first step to financial independence isn't getting out of student loan debt. That's definitely one of the first steps, and HUGE, so I'm not counting it out, but there is something bigger that comes before it: dignity. I found it wonderful that Operation HOPE begins by teaching students about dignity, or "the quality or state of being worthy, honored, or esteemed."

If we have never experienced it -- or really seen it -- do we really feel worthy of financial independence?

That feeling of worth is what drives my desire to succeed, which fuels my desire to learn constantly more about investing, which will help me achieve financial independence.

Over the years, as I've learned more about investing, I've seen more of the ways it enhances wealth in all aspects of society, not just for people. Take your favorite museum, for example. Let's say the Museum of Modern Art. It has an endowment, or a massive investment account that helps them fund the operation.

The endowment is run by professional investors whose primary goal is sustaining the museum's wealth, so it can grow its collection and reach more people. Think about the kids who go to MoMA, whose minds are opened to the world's infinite possibilities, maybe even what they can be when they grow up. A trip to MoMA might a temporary moment of escape for a kid from a not-so-great life situation. To think, the endowment managers get to invest and change lives by supporting the arts for a living -- I can't think of a better career!

To me, investing provides not only a door to financial independence, but to a satisfying career. I want to continue creating and maintaining sustainable wealth for institutional and high net worth investors who are changing thousands of lives. Through this blog, I hope to make my own little mark in the lives of my friends and family. :)

--

In my next post, I'll resume the education: With the bazillions of investing books out there, which ones are actually worth reading?

Sunday, July 28, 2013

'Tis the Season

As investors grow more familiar with the companies in their portfolios, there's a few times a year that build near Christmas-like anticipation: earnings season.

Companies typically report their earnings quarterly. Since they have to get their financial statements audited, checked, and re-checked, there's a slight lag between the end of the quarter (generally the last day of the months of March, June, September, and December) and when earnings are actually reported, so they typically are announced in April, July, October, and January. This is not to say that all companies report during these periods; companies can make up their own fiscal quarters and years if they wish.

Public company earnings are reported, well, publicly. The company CEO or other top management will hold a conference call with investment bankers and institutional investors, and tell them everything the company sold and earned during the quarter. Bankers and investors can ask questions on the call, which can get intense if the company delivers bad news. Retail investors like yourselves can listen to these calls as well, as they might linked to the company's stock listing on Google Finance.

Traditionally, Alcoa, the aluminum producer, is the first company to report, kicking off earnings season for public companies. Investment analysts cling to the company's every word, as they believe that a pattern in Alcoa's reporting may be repeated by other companies, even if they're in a different industry. For example, if Alcoa's earnings go down, and the decline is related to a slowing in construction of homes, analysts can extrapolate that other parts of the economy might slow down, too, from related industries like home improvement retailers (such as Home Depot) or seemingly unrelated ones like PepsiCo (can't forget what sodas come in!).

To that end, earnings season also gives investors an idea of the condition of the overall economy. If companies' earnings are falling across the board, it is likely a sign that consumers are not spending, probably because they can't afford to. If earnings are growing, then the economy is likely on a good curve, going up.

Investors also use a company's earnings announcements to try to predict what's to come in the company's future. For example, Apple's third quarter earnings were announced last week, on July 23. (Click here if you don't have Wall Street Journal access.) The company announced that sales of the iPhone had grown 20% over the past year, but iPad sales dropped 14%. Revenue was basically flat and profits declined 22%. From this information, investors might gather that Apple -- historically an extremely innovative company -- may be losing its edge, especially to competitors like Samsung. Investors show displeasure with earnings results by selling the company's stock, but they didn't sell off Apple very much, showing that they still believe the company can recover.

One thing to note during earnings reports is source, and quality, of earnings. The best reports come from increases in revenues, which lead to increases in net income (profit, or earnings). What we're seeing now overall is companies whose revenues are staying the same, but profits are increasing. This is still good, but could be better. The increase in profits here is coming from decreases in expenses; companies may be cutting back on spending on supplies or even salaries (layoffs!) to save money. This will result in an increase in earnings, but investors want to see growth, not just cost cutting.

While it's not good to obsess or make snap judgments based on one earning's report, I believe that retail investors should pay attention to these announcements and listen to the calls, if possible. If anything, they're a great way to learn more about the company, the closest to an insider's view many of us will ever get. But remember to keep the big picture in the mind: what's going on with the company's competitors? What's going on with the overall economy? In times like these, those questions -- especially the latter -- matter more than anything.

Companies typically report their earnings quarterly. Since they have to get their financial statements audited, checked, and re-checked, there's a slight lag between the end of the quarter (generally the last day of the months of March, June, September, and December) and when earnings are actually reported, so they typically are announced in April, July, October, and January. This is not to say that all companies report during these periods; companies can make up their own fiscal quarters and years if they wish.

Public company earnings are reported, well, publicly. The company CEO or other top management will hold a conference call with investment bankers and institutional investors, and tell them everything the company sold and earned during the quarter. Bankers and investors can ask questions on the call, which can get intense if the company delivers bad news. Retail investors like yourselves can listen to these calls as well, as they might linked to the company's stock listing on Google Finance.

Traditionally, Alcoa, the aluminum producer, is the first company to report, kicking off earnings season for public companies. Investment analysts cling to the company's every word, as they believe that a pattern in Alcoa's reporting may be repeated by other companies, even if they're in a different industry. For example, if Alcoa's earnings go down, and the decline is related to a slowing in construction of homes, analysts can extrapolate that other parts of the economy might slow down, too, from related industries like home improvement retailers (such as Home Depot) or seemingly unrelated ones like PepsiCo (can't forget what sodas come in!).

To that end, earnings season also gives investors an idea of the condition of the overall economy. If companies' earnings are falling across the board, it is likely a sign that consumers are not spending, probably because they can't afford to. If earnings are growing, then the economy is likely on a good curve, going up.

Investors also use a company's earnings announcements to try to predict what's to come in the company's future. For example, Apple's third quarter earnings were announced last week, on July 23. (Click here if you don't have Wall Street Journal access.) The company announced that sales of the iPhone had grown 20% over the past year, but iPad sales dropped 14%. Revenue was basically flat and profits declined 22%. From this information, investors might gather that Apple -- historically an extremely innovative company -- may be losing its edge, especially to competitors like Samsung. Investors show displeasure with earnings results by selling the company's stock, but they didn't sell off Apple very much, showing that they still believe the company can recover.

One thing to note during earnings reports is source, and quality, of earnings. The best reports come from increases in revenues, which lead to increases in net income (profit, or earnings). What we're seeing now overall is companies whose revenues are staying the same, but profits are increasing. This is still good, but could be better. The increase in profits here is coming from decreases in expenses; companies may be cutting back on spending on supplies or even salaries (layoffs!) to save money. This will result in an increase in earnings, but investors want to see growth, not just cost cutting.

While it's not good to obsess or make snap judgments based on one earning's report, I believe that retail investors should pay attention to these announcements and listen to the calls, if possible. If anything, they're a great way to learn more about the company, the closest to an insider's view many of us will ever get. But remember to keep the big picture in the mind: what's going on with the company's competitors? What's going on with the overall economy? In times like these, those questions -- especially the latter -- matter more than anything.

Saturday, July 13, 2013

"Invest in us...Because you're worth it": Alternative Investments

Given the Security and Exchange Commission’s ruling this week

that allows hedge funds and the like to advertise publicly, I can’t think of a

better time to shine some light on what are known as alternative investments.

Alternative investments are called that because, well, they are

alternatives to investing in regular stocks and bonds. Some of the most popular

alternative investments include hedge funds, private equity funds, and venture

capital funds.

Hedge funds

are basically mutual funds for the ridiculously wealthy. A hedge fund pools

money from different people or institutions, and invests in stocks on their

behalf, but the fund doesn’t typically invest the way a mutual fund would. A

hedge fund will invest in derivatives or sell stocks short,

for example.

Private equity funds are similar to hedge funds in that they pool money

from wealthy people and institutions, but these funds don’t buy or sell stocks

that trade on the public markets. They buy whole businesses, sometimes by

buying that company’s stock (which is known as “going private”)

or buying it from its previous owners. Private equity funds generally invest in

businesses with the intention of making them more efficient; after several years,

the fund usually sells the company again, hopefully for a significant profit.

Private equity was talked about which a lot during the 2012 U.S. presidential election, as one of the candidates used to work for a large PE firm. Commercials featuring disgruntled employees he had “fired” from the companies riddled the airwaves. My personal opinion is that the attacks on the PE industry were unfounded and the candidate’s work was taken out of context. Rest assured that PE is not evil; it is very complex, but it is not bad.

Finally, there’s venture capital.

If you watch the ABC show Shark Tank,

you’re already familiar with the concept. Venture capital also pools money from

wealthy investors, but these funds invest in companies that are babies, also

known as start-ups. VC, as it’s known, is widely considered the riskiest of

alternatives because the investments are in companies that are so unsure; many

have not even made a profit yet. But the upside is that you can help an entrepreneur

fulfill a lifelong dream that may be the next Google or Facebook.

All of these investments could potentially make you A LOT of money. But

you know the drill: with high reward comes high risk. These investments are

certainly more risky than buying Treasuries, and are generally more risky than

investing in a stock index fund. BUT, there are a few other stipulations that

make these investments even more out of reach:

- The minimum investment for these funds is typically

$250,000 to $1 million, sometimes more.

-

The fund managers generally get a 20% cut of the

profit AND you have to pay about 2% per year to help them run the fund.

-

Only “accredited” investors

can play in the sandbox anyway.

That being said, if you start to see ads for alternative investments,

most of us can only do just that: watch. But for those who could afford to

play, be cautious, as with any investment, and know what you’re getting

yourself into.

Friday, July 5, 2013

Mutual Fun(d) Decisions: Part 3, IRA What?

Happy

[belated] 4th of July, Readers!

In honor of Independence Day, today, we’ll take a reader question, one that I’m sure more than one person out there has:

In honor of Independence Day, today, we’ll take a reader question, one that I’m sure more than one person out there has:

Dear Stock

Market Chic,

Thank you so

much for the great insights! My investing life will never be the same! Anyway,

I know you’ve talked in previous posts about 401Ks, but I’ve also heard of IRAs

and Roth IRAs. What’s the difference?

Signed,

IRA, what?

Dear IRA,

Thanks for

your question! With so many different investment account acronyms out there, it

can be confusing to get them all sorted, so it’s a great question.

A 401K is a

retirement savings account sponsored by your employer. Money may be taken from

your paycheck pre-tax to help fund it, and the percentage you want to

contribute is typically up to you. Some employers require a certain amount;

others don’t. Either way, you should save as much as you can. Generally, your

employer will match your savings with a certain percentage contribution, too,

but those funds may be off limits until the “vesting period” is over; that is,

you might have to stay with your employer for a certain amount of time in order

to actually get their end of the contribution.

There are limits to how much you

can contribute in a year, though. The

cut-off varies year to year, but is normally somewhere between $15,000 and$17,000, which is a lot to set aside anyway. You decide how to invest your 401K assets,

and none of it is taxed until you take it out of the account. BUT there is a 10%

penalty tax if you take the money out of the account before you’re 59 ½ years

old, on top of the income tax you’d get socked with (there are some legitimate

reasons to not get penalized, though, but they are few and far between). So, to

that end, leave your 401K there until you’re ready to retire, or roll it over

into an IRA.

An IRA, or

individual retirement account, is another type of retirement savings account,

but is not associated with an employer. You can open an IRA at your local bank

or credit union. This account is commonly known as a “traditional” IRA, as

opposed to a Roth, which we’ll discuss in the next section. The biggest thing

to know about traditional IRAs is that they are tax deferred, so you don’t pay

any tax on contributions now, but you will when you withdrawal the funds during

retirement.

Let’s say

you have a 401K at your current job, but you plan to change jobs soon. You can

either keep the 401K where it is or you can roll it over into an IRA. The

latter option allows you to keep contributing to it, tax-deferred. The more you

can shove into a traditional IRA or 401K now, the lower your taxable income

will be, but contribution limits are considerably lower for IRAs, so don’t

think you’re getting over on the IRS. In 2013, it’s $5,500 ($6,500 if you’re

over 50).

A Roth IRA is

almost the exact same thing as a traditional IRA, except that you contribute to

it with after-tax income. Since you’re paying The Man now, you don’t have to

pay him in the future! You might still be subject to a penalty when you

withdrawal the funds, though, depending on your reason for taking the money

out.

That said,

there are strict income limits on Roth contributions, but most people qualify

easily. Maximum contribution also has a bit of a low ceiling, at $5,000, but

you can contribute to a Roth even after you’re retired.

I hope that

clears things up a bit! I’m happy to take more questions!

Wishing you

rich returns,

VonettaFriday, June 28, 2013

Guess I shoulda bought a house last week

Dear Readers,

It's been a while since I've written and a lot has gone on in both my life and the markets! On my end, I graduated from business school, packed up my apt in DC, and moved my whole life to New York City. I've gotten settled in well, exploring the city almost every day. I say "almost" because my job search is in full force, and looking for a job can be a full-time one, ironically. But, I'm back to blogging, so here goes!

---

So much has happened in the markets over the past month, but much of it has occurred in the past week or so. You probably saw headlines to the effect of, "Markets Flinch as Fed Eyes Easy-Money End," or "Global Sell-off Shows Fed Reach Beyond the U.S."

What happened to cause all of this drama?

At a meeting of the Federal Reserve Board, Chairman Ben Bernanke basically said that he is considering ending quantitative easing (the buying up Treasury bonds by the Fed itself to keep interest rates low so people spend and invest more) later this year or at some point next year, rather than waiting until the unemployment rate was below 6.5%, as he initially promised. This implies that Bernanke feels that the U.S. economy is strengthening at a pace that it won't need to be supported by the government anymore; it's a compliment, really.

Problem is, the market did not interpret it as such.

Investors around the world freaked out, selling stocks and bonds like nobody's business, which shows that investors are not as confident in the strength of the U.S. economy as Mr. Bernanke is. It also shows that investors, businesses, and consumers alike have all gotten very used to record low interest rates. (For example, car sales have jumped exponentially over the past year.)

The trouble is, QE has to end at some point. And with that, interest rates will rise. The big sell-off in bonds last week helped them rise already. The yield on 10-year Treasuries jumped to 2.308%, its highest level since March 2012. The yield on 30-year Treasuries rose to 3.65%, a height not seen since 2011. Even more amazingly, these rates went up faster than they have since August 2009.

So, what does that mean for the average individual, even someone who is not an investor?

Treasury yields are used as a base for many interest rates, from savings accounts to car loans to mortgages. With yields being so fickle last week, mortgage rates have shot up. As of June 27, 2013, the rate on 30-year fixed mortgages were 4.46%, the highest since August 2011. BUT, last week, said rate was just 3.93%.

This is really significant because, of course, the interest rate has a massive effect on the size of a mortgage payment. Think of it this way (courtesy of CBS News):

"A $165,000 30-year loan obtained with last week's 3.93 rate will cost $786 per month. Under the new 4.46 percent rate, that jumps to $832 per month. That's a $46 monthly increase -- or a whopping $16,560 over the life of the loan. ...For a $300,000 30-year loan, the rate increase comes to an extra $92 per month, or $33,120 extra over the life of the loan..."

YOWZA!

Unfortunately, there's not much that individual home (or car or appliance) buyers can do. Never try to time the market, of course. Just wish for the best and refinance as appropriate, although the odds of rates doing down from where they are now are extremely slim, in my opinion.

It's been a while since I've written and a lot has gone on in both my life and the markets! On my end, I graduated from business school, packed up my apt in DC, and moved my whole life to New York City. I've gotten settled in well, exploring the city almost every day. I say "almost" because my job search is in full force, and looking for a job can be a full-time one, ironically. But, I'm back to blogging, so here goes!

---

So much has happened in the markets over the past month, but much of it has occurred in the past week or so. You probably saw headlines to the effect of, "Markets Flinch as Fed Eyes Easy-Money End," or "Global Sell-off Shows Fed Reach Beyond the U.S."

What happened to cause all of this drama?

At a meeting of the Federal Reserve Board, Chairman Ben Bernanke basically said that he is considering ending quantitative easing (the buying up Treasury bonds by the Fed itself to keep interest rates low so people spend and invest more) later this year or at some point next year, rather than waiting until the unemployment rate was below 6.5%, as he initially promised. This implies that Bernanke feels that the U.S. economy is strengthening at a pace that it won't need to be supported by the government anymore; it's a compliment, really.

Problem is, the market did not interpret it as such.

Investors around the world freaked out, selling stocks and bonds like nobody's business, which shows that investors are not as confident in the strength of the U.S. economy as Mr. Bernanke is. It also shows that investors, businesses, and consumers alike have all gotten very used to record low interest rates. (For example, car sales have jumped exponentially over the past year.)

The trouble is, QE has to end at some point. And with that, interest rates will rise. The big sell-off in bonds last week helped them rise already. The yield on 10-year Treasuries jumped to 2.308%, its highest level since March 2012. The yield on 30-year Treasuries rose to 3.65%, a height not seen since 2011. Even more amazingly, these rates went up faster than they have since August 2009.

So, what does that mean for the average individual, even someone who is not an investor?

Treasury yields are used as a base for many interest rates, from savings accounts to car loans to mortgages. With yields being so fickle last week, mortgage rates have shot up. As of June 27, 2013, the rate on 30-year fixed mortgages were 4.46%, the highest since August 2011. BUT, last week, said rate was just 3.93%.

This is really significant because, of course, the interest rate has a massive effect on the size of a mortgage payment. Think of it this way (courtesy of CBS News):

"A $165,000 30-year loan obtained with last week's 3.93 rate will cost $786 per month. Under the new 4.46 percent rate, that jumps to $832 per month. That's a $46 monthly increase -- or a whopping $16,560 over the life of the loan. ...For a $300,000 30-year loan, the rate increase comes to an extra $92 per month, or $33,120 extra over the life of the loan..."

YOWZA!

Unfortunately, there's not much that individual home (or car or appliance) buyers can do. Never try to time the market, of course. Just wish for the best and refinance as appropriate, although the odds of rates doing down from where they are now are extremely slim, in my opinion.

Monday, May 6, 2013

Thoughts on Current Market Events

So, you might have seen the headline last week: “Markets

Soar to New Highs.” Or, “Job Gains Calm Slump Worries.”

The Dow Jones Industrial Average, the index that tracks the 30 largest companies in the US, hit an all-time high, above 15,000, on Friday, as did the S&P 500, which flew to over 1,600 points. (Think of “points” as the price per share of this exact index, which is very different from that of a fund or ETF that reflects the index.)

Ordinarily, this would be time for great rejoicing. If you have an index fund, it is likely performing extraordinarily well and you have no complaints at all. Companies’ earnings reports have been generally positive, although many companies are missing analysts’ estimates.

So what’s the big deal?

A) The big deal is the big picture: although unemployment has been falling, it is still 7.6%, which is higher than the targeted 6.5% and much higher than the historical average of 5.8% (the historical average is only this high because it is taking the past five years into account, when the rate reached over 10%).

U.S. Treasury yields are still at near-historical lows, with the 30-year bond – traditionally the highest yielding – at 2.98%. Some blame quantitative easing for keeping these yields so low. Quantitative easing involves the Federal Reserve buying U.S. Treasuries, with the purpose of keeping yields low so it is cheaper for companies (and individuals) to borrow money to buy houses, cars, etc. The central bank began QE in 2009 and has said that it would stop when the unemployment rate reached 6.5%.

As a result, investors who would typically rely on Treasuries for yield have not been able to make the money they sought to with yields as low as they are. So, they began buying stocks. And more stocks. And more stocks. And even more stocks, pushing the price up to 15,000 and 1,600 for the DJIA and S&P, respectively.

Some investors are now nervous because they think the market is overbought and overvalued. Well, the S&P 500’s historical price-earnings ratio is about 15. Right now, it’s nearly 19. So, yes, the market may be a little overvalued.

B) Another explanation for the recent surge is that investors are anticipating stronger growth in the U.S. economy quite soon. One way that stock prices are determined is by calculating the present value of a company’s future earnings. One could say that the U.S. economy’s future earnings look so great right now that the high market price is deserved. Optimism!

I’m inclined to go with option A, based on my education. Although I am very optimistic about the outlook of the U.S. economy, I think sending the market to new highs on an uncertain foundation is not sound. I would advise my friends to hold off on stock purchases until the market cools down. However, I’m no Miss Cleo and I could be wrong (actually, that would make me a Miss Cleo, haha!).

The Dow Jones Industrial Average, the index that tracks the 30 largest companies in the US, hit an all-time high, above 15,000, on Friday, as did the S&P 500, which flew to over 1,600 points. (Think of “points” as the price per share of this exact index, which is very different from that of a fund or ETF that reflects the index.)

Ordinarily, this would be time for great rejoicing. If you have an index fund, it is likely performing extraordinarily well and you have no complaints at all. Companies’ earnings reports have been generally positive, although many companies are missing analysts’ estimates.

So what’s the big deal?

A) The big deal is the big picture: although unemployment has been falling, it is still 7.6%, which is higher than the targeted 6.5% and much higher than the historical average of 5.8% (the historical average is only this high because it is taking the past five years into account, when the rate reached over 10%).

U.S. Treasury yields are still at near-historical lows, with the 30-year bond – traditionally the highest yielding – at 2.98%. Some blame quantitative easing for keeping these yields so low. Quantitative easing involves the Federal Reserve buying U.S. Treasuries, with the purpose of keeping yields low so it is cheaper for companies (and individuals) to borrow money to buy houses, cars, etc. The central bank began QE in 2009 and has said that it would stop when the unemployment rate reached 6.5%.

As a result, investors who would typically rely on Treasuries for yield have not been able to make the money they sought to with yields as low as they are. So, they began buying stocks. And more stocks. And more stocks. And even more stocks, pushing the price up to 15,000 and 1,600 for the DJIA and S&P, respectively.

Some investors are now nervous because they think the market is overbought and overvalued. Well, the S&P 500’s historical price-earnings ratio is about 15. Right now, it’s nearly 19. So, yes, the market may be a little overvalued.

B) Another explanation for the recent surge is that investors are anticipating stronger growth in the U.S. economy quite soon. One way that stock prices are determined is by calculating the present value of a company’s future earnings. One could say that the U.S. economy’s future earnings look so great right now that the high market price is deserved. Optimism!

I’m inclined to go with option A, based on my education. Although I am very optimistic about the outlook of the U.S. economy, I think sending the market to new highs on an uncertain foundation is not sound. I would advise my friends to hold off on stock purchases until the market cools down. However, I’m no Miss Cleo and I could be wrong (actually, that would make me a Miss Cleo, haha!).

Wednesday, April 24, 2013

401K/403B Mutual Fun(d) Decisions: Part 2, Fund Allocations

*My apologies for the brevity of this post. I’m feeling terribly under

the weather (thanks, DC, for being 80 degrees one day and 40 the next). More on

this topic to come.

Now that we’ve gotten what fees and expenses to look for out of the way, it’s time to talk actual funds. Please note again that I am not an investment professional (yet!) and can only educate on the types of funds out there. I’m not selling funds until I get some commission. ;)

For starters, you already know about equity (or, stock) funds and bond funds. (More on bonds in a future post.) Depending on the financial advisor, advice will range from “go 100% equity” for young people to “keep it 50/50 stocks/bonds.” As stated in previous posts, your choice depends on your risk tolerance, but know that risk aversion, or a very high allocations to bonds, can lower your returns potential over time.

That said, look for stock funds that have the broadest range of stocks possible, like an index fund that reflects the S&P 500 or Wilshire 5000. If you find an index fund that has every stock available (more than 5,000), go for it, for maximum equity diversification.

Next, throw in a good mix of U.S. Treasury, and maybe corporate, bonds. The longer the maturity, or length of time until you get the principal amount back, the higher the yield, to compensate you for the risk you’ve taken of giving your money to the government for such a long time (the longest maturity available for U.S. Treasury bonds is 30 years).

Don’t forget international stocks and bonds! They provide great diversification to a U.S. investor’s portfolio.

I recommend finding index funds for all of these asset classes. If you have to go with an actively managed fund (as you would have to do for bond funds), go with one with low fees and high ratings on Morningstar.com, a well-respected finance research website.

Now that we’ve gotten what fees and expenses to look for out of the way, it’s time to talk actual funds. Please note again that I am not an investment professional (yet!) and can only educate on the types of funds out there. I’m not selling funds until I get some commission. ;)

For starters, you already know about equity (or, stock) funds and bond funds. (More on bonds in a future post.) Depending on the financial advisor, advice will range from “go 100% equity” for young people to “keep it 50/50 stocks/bonds.” As stated in previous posts, your choice depends on your risk tolerance, but know that risk aversion, or a very high allocations to bonds, can lower your returns potential over time.

That said, look for stock funds that have the broadest range of stocks possible, like an index fund that reflects the S&P 500 or Wilshire 5000. If you find an index fund that has every stock available (more than 5,000), go for it, for maximum equity diversification.

Next, throw in a good mix of U.S. Treasury, and maybe corporate, bonds. The longer the maturity, or length of time until you get the principal amount back, the higher the yield, to compensate you for the risk you’ve taken of giving your money to the government for such a long time (the longest maturity available for U.S. Treasury bonds is 30 years).

Don’t forget international stocks and bonds! They provide great diversification to a U.S. investor’s portfolio.

I recommend finding index funds for all of these asset classes. If you have to go with an actively managed fund (as you would have to do for bond funds), go with one with low fees and high ratings on Morningstar.com, a well-respected finance research website.

Wednesday, April 17, 2013

401K/403B Mutual Fun(d) Decisions: Part 1, Expenses

Anyone my age or younger will probably never know what a corporate pension looks like. And, sadly, Social Security will have likely run out by the time we retire. So, saving for retirement is a burden we bare all to ourselves. Employers try to help by offering 401Ks or 403Bs, but this gets overwhelming when there are typically approximately 80,000,000,000 mutual funds and ETFs to choose from.

How do you know a good fund from a bad one?

What the hell is the difference between a "core value" fund and a "large cap blend" fund, anyway?

Should you go for gold, just because a metals and mining fund is available?

Don't pull your hair out over your 401K. Remember that it's there to help you. Over the next couple of posts, we'll talk through some high-level details to consider when selecting funds for your portfolio.

--

One of the biggest things to keep in mind are fees and expenses. These dollars can set the best of funds apart from the worst because of simple math: the more you pay in fees, the more your investment has to return to make up for those fees. God only knows that you don't want to just go around giving your money away for free. So, here are some brief explanations of the fees you'd typically see from mutual funds.

Mutual funds will typically have 4 types of expenses: operating expenses, a front-end load, a back-end load, and a 12b-1 fee.

Operating Expenses

Operating expenses are costs necessary to run the fund. Fund managers have to pay electricity bills like the rest of us, plus employee salaries. Operating expenses are generally hard to get around because they're just a part of doing business.

These fees can be as low as .06% (also known as 6 basis points) of invested assets and as high as 1.5% or greater. Index funds generally have the lower fees, as it doesn't take as much work on the part of the fund manager to run the fund, since it is supposed to just be a reflection of an existing stock or bond index. You might also see this style of investing called passive management. It's sister, active management, is much more expensive. Actively managed funds are typically trying to outperform the overall market or a certain index by investing in specific stocks. In order to do that, fund managers are much more involved in the fund, handpicking stocks or bonds. As a result, these funds wind up being much more expensive; unfortunately, they don't always meet their goal of beating the market, either, meaning that investors are charged more for worse performance, potentially.

My advice to you is to go for a passive index fund that will reflect an index like the S&P 500, or even better, every stock in the market (more on that next week) for lower expenses.

Loads

Now, the front- and/or back-end loads, on the other hand, are not so necessary. A "load" is basically a sales fee charged to you when you first buy the mutual fund ("front-end" load) or when you sell, or redeem it ("back-end" load). Then there are no-load funds, mostly from a company called Vanguard, which is extremely well respected in the finance community.

These expenses can run from 0% to 8.5%. The load is especially important to note because it can be total robbery of your investment. When you pay a load, especially a front-end load, you really are just giving your money to a fund manager and not asking for it back. You do expect for the return on your investment to be greater than the load, but you've put yourself farther in the hole from the start.

Example from my own life (glad I learned these things the hard way, so you don't have to!). When I switched jobs to my last job before business school, I rolled over my previous 401K into an IRA (we'll talk about those later, too). I was curious about active management, so my retirement advisor at my bank recommended that I go with a Goldman Sachs fund that had a 5.25% load. I started with about $4,000. After the load, I was only investing $3,800. I needed the fund to return me my $200 (AT LEAST), plus the 1.25% annual expense.

Let's just say, after the market spun itself around in 2010 and 2011, I was lucky to finish right back where I "started," with $3,800. I could have lost much more. But had I invested in an index fund that reflected the S&P 500 with a no-load fund, I would have gained about 15% over that same time period. You live and learn.

12b-1 Fees

12b-1 fees are optional fees the fund can charge so investors pay for part of the fund's advertising costs. Funds do charge them, but again, if there's no need to just give your money away and dig yourself further into a hole, don't do it.

--

So, now you know some the key expenses to look for when selecting a mutual fund. (Remember to go cheap!) Next week, we'll look at some of the types of funds that will help you diversify and grow your retirement savings.

How do you know a good fund from a bad one?

What the hell is the difference between a "core value" fund and a "large cap blend" fund, anyway?

Should you go for gold, just because a metals and mining fund is available?

Don't pull your hair out over your 401K. Remember that it's there to help you. Over the next couple of posts, we'll talk through some high-level details to consider when selecting funds for your portfolio.

--

One of the biggest things to keep in mind are fees and expenses. These dollars can set the best of funds apart from the worst because of simple math: the more you pay in fees, the more your investment has to return to make up for those fees. God only knows that you don't want to just go around giving your money away for free. So, here are some brief explanations of the fees you'd typically see from mutual funds.

Mutual funds will typically have 4 types of expenses: operating expenses, a front-end load, a back-end load, and a 12b-1 fee.

Operating Expenses

Operating expenses are costs necessary to run the fund. Fund managers have to pay electricity bills like the rest of us, plus employee salaries. Operating expenses are generally hard to get around because they're just a part of doing business.

These fees can be as low as .06% (also known as 6 basis points) of invested assets and as high as 1.5% or greater. Index funds generally have the lower fees, as it doesn't take as much work on the part of the fund manager to run the fund, since it is supposed to just be a reflection of an existing stock or bond index. You might also see this style of investing called passive management. It's sister, active management, is much more expensive. Actively managed funds are typically trying to outperform the overall market or a certain index by investing in specific stocks. In order to do that, fund managers are much more involved in the fund, handpicking stocks or bonds. As a result, these funds wind up being much more expensive; unfortunately, they don't always meet their goal of beating the market, either, meaning that investors are charged more for worse performance, potentially.

My advice to you is to go for a passive index fund that will reflect an index like the S&P 500, or even better, every stock in the market (more on that next week) for lower expenses.

Loads

Now, the front- and/or back-end loads, on the other hand, are not so necessary. A "load" is basically a sales fee charged to you when you first buy the mutual fund ("front-end" load) or when you sell, or redeem it ("back-end" load). Then there are no-load funds, mostly from a company called Vanguard, which is extremely well respected in the finance community.

These expenses can run from 0% to 8.5%. The load is especially important to note because it can be total robbery of your investment. When you pay a load, especially a front-end load, you really are just giving your money to a fund manager and not asking for it back. You do expect for the return on your investment to be greater than the load, but you've put yourself farther in the hole from the start.

Example from my own life (glad I learned these things the hard way, so you don't have to!). When I switched jobs to my last job before business school, I rolled over my previous 401K into an IRA (we'll talk about those later, too). I was curious about active management, so my retirement advisor at my bank recommended that I go with a Goldman Sachs fund that had a 5.25% load. I started with about $4,000. After the load, I was only investing $3,800. I needed the fund to return me my $200 (AT LEAST), plus the 1.25% annual expense.

Let's just say, after the market spun itself around in 2010 and 2011, I was lucky to finish right back where I "started," with $3,800. I could have lost much more. But had I invested in an index fund that reflected the S&P 500 with a no-load fund, I would have gained about 15% over that same time period. You live and learn.

12b-1 Fees

12b-1 fees are optional fees the fund can charge so investors pay for part of the fund's advertising costs. Funds do charge them, but again, if there's no need to just give your money away and dig yourself further into a hole, don't do it.

--

So, now you know some the key expenses to look for when selecting a mutual fund. (Remember to go cheap!) Next week, we'll look at some of the types of funds that will help you diversify and grow your retirement savings.

Wednesday, April 3, 2013

Can you risk it?

My great aunt had a way with words. Among her best quotes are, "Love is good, but money's better," "Love don't pay the rent," and "Don't marry a man if he don't have a key to something." (Great advice on all fronts.) Once, my sister told her about a guy she'd started dating, and my aunt wanted know if the guy was trustworthy. Instead of asking, "Do you trust him?," she said, "Can you risk him?"

She wasn't all wrong in correlating risk and trust. It's hard to trust the market, since you know it flucurates so much, so it all comes down to how much you stomach.

The first thing to know and remember like your own name is that there is no such thing as a risk-free investment. (Although U.S. Treasuries are called "risk-free" because they are backed by the government, their value is still at risk of being eaten away by inflation. And, it doesn't seem all that possible, but the government could default one day.)

So, if anyone ever offers you an investment opportunity that has "no risk," RUN AWAY because it is a scam.

That said, the amount of flucuation you can stomach is known as your risk tolerance. To help determine your level of tolerance, there are a ton of quizzes you can take. A couple of ones that I found legitimate were from Merrill Lynch and Rutgers University. The one from Merrill focuses solely on investment decisions, while the Rutgers one -- since it is actually a study on risk behavior -- is more broad and user-friendly, in my opinion.

Quizzes like these present you with questions that try to get at how much you are willing to lose for the chance of making gains. It may surprise you how much the magnitude of the potential gain matters versus the magnitude of potential loss. (I won't give it away; I'll let you take the quiz and find out for yourself!)

Some general rules/thoughts regarding risk are:

*Source: Google Finance S&P 500 chart.

She wasn't all wrong in correlating risk and trust. It's hard to trust the market, since you know it flucurates so much, so it all comes down to how much you stomach.

The first thing to know and remember like your own name is that there is no such thing as a risk-free investment. (Although U.S. Treasuries are called "risk-free" because they are backed by the government, their value is still at risk of being eaten away by inflation. And, it doesn't seem all that possible, but the government could default one day.)

So, if anyone ever offers you an investment opportunity that has "no risk," RUN AWAY because it is a scam.

That said, the amount of flucuation you can stomach is known as your risk tolerance. To help determine your level of tolerance, there are a ton of quizzes you can take. A couple of ones that I found legitimate were from Merrill Lynch and Rutgers University. The one from Merrill focuses solely on investment decisions, while the Rutgers one -- since it is actually a study on risk behavior -- is more broad and user-friendly, in my opinion.

Quizzes like these present you with questions that try to get at how much you are willing to lose for the chance of making gains. It may surprise you how much the magnitude of the potential gain matters versus the magnitude of potential loss. (I won't give it away; I'll let you take the quiz and find out for yourself!)

Some general rules/thoughts regarding risk are:

- If you're younger, you can take more risks. This is because of precious time your portfolio will have to recover from market losses. For example, if you'd invested $100 in the market on January 7, 2000, by December 27, 2002, you would have lost almost $41 dollars. Let's say you decided to hold on to those shares instead of selling them at a loss.* By December 28, 2007, you would have recovered your losses.* Holding for a brief period (that, in this example, was a terrible time for the market overall) would not have served you well, but over a longer period of time, you actually gain.

- Small-cap stocks tend to be riskier than medium- and large-cap stocks. This is because small-cap stocks are from smaller companies that are not as established, but have a lot of growth potential. Take Rocky Mountain Chocolate Factory, which operates in malls, primarily, in 40 states, Canada, Japan, and the UAE. This company is growing in different geographies, but since chocolate is not a commodity, its business can flucuate in hard economic times, so this investment would certainly be riskier than one in Hershey, for example, since the latter has been around for 100 years or so and has a strong global presence.

- Women tend to take fewer risks when investing. Common thought holds that women tend to be more risk averse when it comes to investing. Which could mean that a woman's retirement savings will likely be much lower than her male counterpart's. However, loss aversion can be useful. Women may be more inclined to make more thoughtful investment choices than men and stay out of overly risky investments. Some say that if more women were on the boards of banks, the financial crisis would never have happened.

- Stocks tend to outperform bonds. Historically, stocks have consistently outperformed bonds over time. From 1928 to 2012, the S&P 500 beat out ten-year Treasuries by more than 3 percentage points, which could be the difference between making $871 or $564 off of a $100 investment. It's good to have a diversified portfolio of stocks and bonds that complement each other, but stocks tend to have greater upside potential. Since bonds are debt, the bondholders, like a credit card company, are ultimately more concerned with getting their money back rather than what can be made on top of it. Equityholders, on the other hand, do not have to be paid back, so upside is all they can hope for; in exchange for taking on this risk, they get a higher reward. Get rewarded for holding stocks!

*Source: Google Finance S&P 500 chart.

Wednesday, March 27, 2013

Investing in Emerging Markets: Growth for your portfolio and the world over

Today we're going to talk about investing in emerging markets, what exactly that means, how to do it, and some of the risks involved.

First, let's get out of the way what emerging markets are: developing economies that may still have relatively high rates of poverty, but are growing rapidly. Examples include China, India, Brazil, Mexico, and South Africa. (For the sake of comparison, countries such as the U.S., Canada, U.K., France, Germany, and the like are all considered "developed.")

There are also "frontier markets," which are even riskier than emerging markets because they are generally less economically and politically stable, but still have potential to grow into emerging, or even developed, nations. These include countries such as Argentina, Ghana, Colombia, and Vietnam.

The key thing to note about emerging and frontier markets is their incredible growth potential. In the early part of the past decade, investors were lured by these countries' huge economic growth rates, anywhere from 7% to 10% per year or more. In contrast, the U.S.'s and other developed economies' gross domestic products (GDP) only grow about 3% per year, and that's during a good year. (GDP is typically what people are referring to when they talk about the "economy" more broadly. It's basically the value of all the goods and services made in the country.)

While the global financial crisis slowed almost all countries' economies, some emerging nations proved more resilient. For example, although China's growth has slowed, it is still grew more than 7% in 2012 (compare to the U.S., which grew only about 2%. Final numbers on U.S. GDP growth for 2012 will be out soon).

Because of this outstanding growth potential, investors stand to make a ton of money. Think about it: think about people who invested in U.S. railroads, for example, in the 1800s -- those families are still wealthy today! Emerging and frontier markets investors can take essentially the same stance. Incredible!

However, where there is significant reward, there is significant risk. Note again some of the countries I mentioned: Mexico, Argentina, Vietnam. While they make for great adventure vacation spots, they are not known for being the most politically stable. Democracy and capitalism are working their way around the world, but in many places, governments control (and often inhibit) countries' growth. This adds a lot of risk for investors.

For example, let's say an investor has found a way to fund infrastructure building in Argentina, but new government leadership comes in and decides that alleviating proverty through social programs will be the new priority and all infrastructure building will come to a halt. Panicked, the investor looks to sell her investment, but no one wants to buy it now that everyone knows that infrastructure has gone kaput. During all of this, the value of Argentina's currency declines, so she now owns even more of an investment that no one wants. So, the value of the investment tanks and the investor loses her money.

This is a very elementary (and likely unrealistic for Argentina) example, but I want to highlight exactly how risky investing in emerging and frontier markets can be. Not only are there the risks we discussed previously about individual companies, but there are also political and currency risks.

Know that investments in other countries will likely be made in that country's currency, not in U.S. dollars, so there may be money gained or lost during the translation. Additionally, one has to pay taxes on these investments as well, which will eat into returns even more. These investments can also be less liquid, or harder to sell, than developed markets equities (stocks).

So why on earth would anyone invest in emerging markets after all that?

Because of faith in the growth stories.

Emerging markets investors get to be a part of helping build roads, factories, and maybe even schools around the world, giving people jobs, educations, and livelihoods. And, as I mentioned earlier, these countries generally grow much more rapidly than the U.S., so investment values go up very quickly. They also tend to go up when U.S. equities go down, and vice versa, so they can add a layer of diversification to a U.S.-based stock portfolio. (This excludes recent times of economic decline around the world. We live in a very unique time that I pray will get much better soon.)

So, if you are not overly risk averse, and if you are young, then you should be investing in emerging and/or frontier markets. As stated in previous posts, time has a way of ironing out wrinkles brought on by volatility.

If you have a 401k or 403b, see if there is a mutual fund that invests specifically in emerging and/or frontier markets and add it to your portfolio. You can also likely find index funds or ETFs from your brokerage to invest in, such as the Schwab Emerging Markets Equity ETF.

Only make these investments if they fit your risk appetite. Next week, we'll talk more about risk and how to determine how much of it you can stomach.

First, let's get out of the way what emerging markets are: developing economies that may still have relatively high rates of poverty, but are growing rapidly. Examples include China, India, Brazil, Mexico, and South Africa. (For the sake of comparison, countries such as the U.S., Canada, U.K., France, Germany, and the like are all considered "developed.")

There are also "frontier markets," which are even riskier than emerging markets because they are generally less economically and politically stable, but still have potential to grow into emerging, or even developed, nations. These include countries such as Argentina, Ghana, Colombia, and Vietnam.

The key thing to note about emerging and frontier markets is their incredible growth potential. In the early part of the past decade, investors were lured by these countries' huge economic growth rates, anywhere from 7% to 10% per year or more. In contrast, the U.S.'s and other developed economies' gross domestic products (GDP) only grow about 3% per year, and that's during a good year. (GDP is typically what people are referring to when they talk about the "economy" more broadly. It's basically the value of all the goods and services made in the country.)

While the global financial crisis slowed almost all countries' economies, some emerging nations proved more resilient. For example, although China's growth has slowed, it is still grew more than 7% in 2012 (compare to the U.S., which grew only about 2%. Final numbers on U.S. GDP growth for 2012 will be out soon).

Because of this outstanding growth potential, investors stand to make a ton of money. Think about it: think about people who invested in U.S. railroads, for example, in the 1800s -- those families are still wealthy today! Emerging and frontier markets investors can take essentially the same stance. Incredible!

However, where there is significant reward, there is significant risk. Note again some of the countries I mentioned: Mexico, Argentina, Vietnam. While they make for great adventure vacation spots, they are not known for being the most politically stable. Democracy and capitalism are working their way around the world, but in many places, governments control (and often inhibit) countries' growth. This adds a lot of risk for investors.

For example, let's say an investor has found a way to fund infrastructure building in Argentina, but new government leadership comes in and decides that alleviating proverty through social programs will be the new priority and all infrastructure building will come to a halt. Panicked, the investor looks to sell her investment, but no one wants to buy it now that everyone knows that infrastructure has gone kaput. During all of this, the value of Argentina's currency declines, so she now owns even more of an investment that no one wants. So, the value of the investment tanks and the investor loses her money.

This is a very elementary (and likely unrealistic for Argentina) example, but I want to highlight exactly how risky investing in emerging and frontier markets can be. Not only are there the risks we discussed previously about individual companies, but there are also political and currency risks.

Know that investments in other countries will likely be made in that country's currency, not in U.S. dollars, so there may be money gained or lost during the translation. Additionally, one has to pay taxes on these investments as well, which will eat into returns even more. These investments can also be less liquid, or harder to sell, than developed markets equities (stocks).

So why on earth would anyone invest in emerging markets after all that?

Because of faith in the growth stories.

Emerging markets investors get to be a part of helping build roads, factories, and maybe even schools around the world, giving people jobs, educations, and livelihoods. And, as I mentioned earlier, these countries generally grow much more rapidly than the U.S., so investment values go up very quickly. They also tend to go up when U.S. equities go down, and vice versa, so they can add a layer of diversification to a U.S.-based stock portfolio. (This excludes recent times of economic decline around the world. We live in a very unique time that I pray will get much better soon.)

So, if you are not overly risk averse, and if you are young, then you should be investing in emerging and/or frontier markets. As stated in previous posts, time has a way of ironing out wrinkles brought on by volatility.

If you have a 401k or 403b, see if there is a mutual fund that invests specifically in emerging and/or frontier markets and add it to your portfolio. You can also likely find index funds or ETFs from your brokerage to invest in, such as the Schwab Emerging Markets Equity ETF.

Only make these investments if they fit your risk appetite. Next week, we'll talk more about risk and how to determine how much of it you can stomach.

Wednesday, March 20, 2013

Investing Insights from China

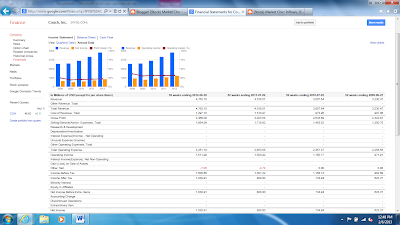

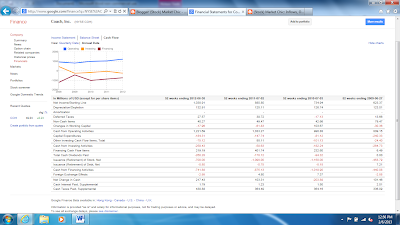

I'm back from the trip of a lifetime in China. While it was an interesting experience for many reasons (primarily because I'm African-American and was quite the spectacle, apparently), I learned ton more about how business is done in China and I know understand much more why investors get so jazzed about sending money to the East.

Upon arrival in Shanghai, I was greeted by this huge Coach ad, right outside my hotel window:

Upon arrival in Shanghai, I was greeted by this huge Coach ad, right outside my hotel window:

It is a country of both extreme wealth and extreme poverty, but investors have jumped on the former as a money-making opportunity. The Chinese middle class is burgeoning and, like Western countries, this means that the population is consuming more luxury goods. I saw an impressive number of Coach, Tiffany, and Louis Vuitton stores in Shanghai alone.

But, before you march off to buy shares, note one thing. Many purchases of luxury goods in China were the result of a business and government culture of gifting. Some might call it "bribing," but I think that's too strong a term. Business partners exchange gifts after a deal is closed as a way to thank each other for doing the transaction. Following my team's presentation, we gave our company representatives small tokens of our appreciation, and the they did the same for us. Of course this can lead to many abuses, especially bribing. To that end, the Chinese government is cracking down on this type of corruption. Unfortunately, this may take an unforseen toll on luxury brands in China. A new government was inaugurated only in the last few weeks, so only time will tell what will actually happen. But investors in luxury goods companies who are relying on growth in China should beware.

Another thing to note is the major housing boom in the big cities, especially Shanghai, Beijing, and Xi'an. China is the world's most populous country with 1.36 billion people, and all of those people need to live somewhere. However, I was taken aback at the rapid real estate development. It seemed to me that houses (well, apartments, mostly, as result of high population density) were being built long before demand could fill them. This could also play a role in the future on the incomes of the Chinese middle class. If housing values fall, so will their net worths and ability to spend on luxury items. The Communist government can likely keep some damage from occuring if there is a bubble burst like that of the US in 2007. But I would caution investors to be careful of a situation that appears to be growing more precarious.

It's not all bad news, of course! I saw a lot of growth potential in China, particularly in terms of infrastructure. As they continue to build homes, they will need roads, electricity, and public transportation. There is also a bit of a pollution problem that will have to be tackled. Investors can take advantage of these things by putting money toward building out these roads and investing in companies that will put electrical wires underground. Some of my classmates also joked that, once it becomes required to wear a bike helmet, helmet makers will clean up!

Some people say that China is "out," as if it were culottes or harem pants. The world's largest nation definitely has opporunities, but I would shake things up a bit by looking at Brazil or India, or in even riskier frontier markets, such as Mexico. Next week, I'll explore how one would invest in emerging markets.

Thursday, February 28, 2013

The globe is calling me...

Dearest Readers,

You didn't miss a post from me yesterday -- I was getting ready for a big trip! I'm headed to China tomorrow for my MBA program's Global Residency in Shanghai, where I'll be meeting with bigwigs and making a presentation to the heads of a Chinese financial services company. Wish me luck!

Posts will resume on March 20, after I've returned.

Wishing you rich returns,

Vonetta

You didn't miss a post from me yesterday -- I was getting ready for a big trip! I'm headed to China tomorrow for my MBA program's Global Residency in Shanghai, where I'll be meeting with bigwigs and making a presentation to the heads of a Chinese financial services company. Wish me luck!

Posts will resume on March 20, after I've returned.

Wishing you rich returns,

Vonetta

Wednesday, February 20, 2013

A diverse world is a safe(r) world

And by "world" I, of course, mean your stock portfolio.

So far, in each blogpost, I've explained the basics of what you need to know to buy the stock of an individual company. Although you do need to know this, a more important [and very familiar] principle stands:

Avoid putting all your eggs in one basket.

This principle is known as diversification. Basically, it involves owning a number of stocks of companies in different industries, geographies, etc etc. You might hear the rule that a properly diversified investment portfolio contains 30 to 40 stocks, which you can gather yourself OR you can let someone else do it for you, with a mutual fund or an exchange-traded fund.

A mutual fund is a diverse portfolio of stocks (or bonds) that is managed by an asset management firm. The "mutual" part comes from the fact that it is funded by a ton of different people. Money is pooled from many different investors and the asset manager invests on their behalf.

If your job offers you a 401k or 403b plan, you have likely bought a mutual fund. It is one of the easiest, best ways to get a diversified portfolio, since these funds can include hundreds, or even thousands, of stocks.

Another way to get diversity is through an exchange-traded fund, more widely known as an ETF. ETFs work essentially the same way as a mutual fund, but is traded on an exchange, such as the New York Stock Exchange. Mutual funds are not publicly traded, so an ETF can be more convenient for those who do not have access to a 401k plan.

Both mutual funds and ETFs give you about a million investing options. Some funds invest companies in one industry specifically; some invest based on geographies. Some reflect popular indices such as the Dow Jones Industrial Average or the S&P 500, called index funds.

Conservative Wall Street veterans will likely recommend that you go with an index fund, particularly one that includes more companies rather than fewer. While the Dow's price is frequently quoted, the index is made up of only 30 stocks, the largest companies in the US. Bigger isn't always better: these companies don't necessarily reflect what's going on in the whole market. The S&P 500, which contains 500 companies' stocks, is a better bet, and the Wilshire 5000, even better.

So next time you're tinkering with your job's 401k, don't be shy. See what index funds are available. Next time, I'll teach out how to seek out the best for you.

So far, in each blogpost, I've explained the basics of what you need to know to buy the stock of an individual company. Although you do need to know this, a more important [and very familiar] principle stands:

Avoid putting all your eggs in one basket.

This principle is known as diversification. Basically, it involves owning a number of stocks of companies in different industries, geographies, etc etc. You might hear the rule that a properly diversified investment portfolio contains 30 to 40 stocks, which you can gather yourself OR you can let someone else do it for you, with a mutual fund or an exchange-traded fund.

A mutual fund is a diverse portfolio of stocks (or bonds) that is managed by an asset management firm. The "mutual" part comes from the fact that it is funded by a ton of different people. Money is pooled from many different investors and the asset manager invests on their behalf.

If your job offers you a 401k or 403b plan, you have likely bought a mutual fund. It is one of the easiest, best ways to get a diversified portfolio, since these funds can include hundreds, or even thousands, of stocks.

Another way to get diversity is through an exchange-traded fund, more widely known as an ETF. ETFs work essentially the same way as a mutual fund, but is traded on an exchange, such as the New York Stock Exchange. Mutual funds are not publicly traded, so an ETF can be more convenient for those who do not have access to a 401k plan.